Long Term Wealth Planning

Long Term Wealth Planning

Imagine yourself, just a college pass-out with hundreds of dreams and a job offer in hand. You joined the company, worked hard, and received your 1st salary in your account. Whatever the amount is, this feeling holds a separate value in everyone’s life.

You might have already planned what to do with that amount — paying rent, purchasing something for your family, or gifting something to yourself with your first hard-earned money. But how about starting an investment or to be more precise – Financial planning?

Many people do not even think about investing in their initial earning phase because they feel that they have enough time for it and can start later as well.

What actually is Long-Term Wealth Planning?

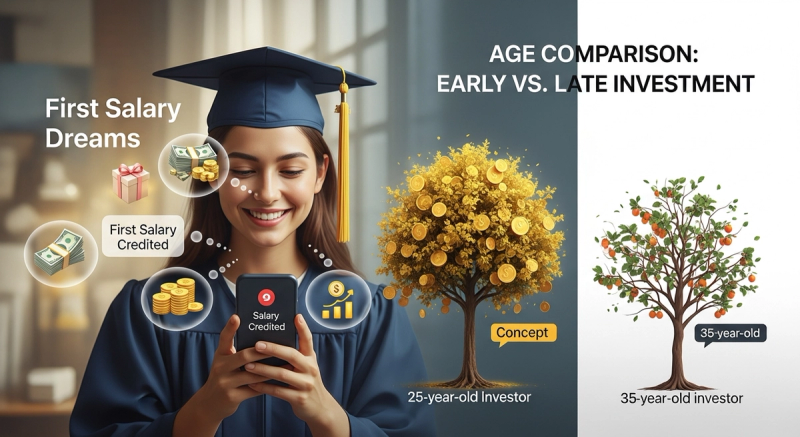

Wealth planning can be started with Financial discipline and good intentions towards your money. You can surely compare the corpus of a person who started investing at the age of 25 with someone else who started investing at the age of 35. The difference will be surprisingly higher for the person who started early.

This difference is due to the power of compounding. It has already been said by Mr. Albert Einstein that compound interest is the eighth wonder of the world, and the mathematics behind this logic also cannot be denied.

Starting Now – Steps to Check

Step 1 (Where do you find yourself standing?)

Start with the calculations part — how much is my monthly in-hand salary, how much are my expenses, some part kept for an emergency fund, and then comes what is left at the end of the month. A part of that amount is something you can think of investing.

Step 2 (Building the emergency fund)

This is the first thing you should do. Although there is no such fixed figure that you should have in your bank account as your emergency fund, but roughly around 4–6 months of your monthly expenses is considered good.

See, today’s scenario is quite unpredictable. We cannot even imagine how things may change even in just 1 day. A person working in a Big 4 company today could be jobless tomorrow. We have heard people saying, “Don’t think about bad things,” but we have to be ready for the worst.

So, before building anything else, create this foundation of an emergency fund on which you can rely.

Step 3 (Understand what compounding is)

One general example from our daily life — everyone will agree on this:

Doing:

- 10 pushups once = no visible change

- 10 pushups daily for 1 year = huge transformation

So, compounding means that small actions or amounts done consistently can create massive results over time.

Now relate it with a SIP calculation —

Let’s say you have started investing ₹5,000 per month at the age of 25 in a mutual fund giving returns of around 12% annually on average.

So, by the time you reach 55, your corpus will stand somewhere around ₹1.7 Cr with an investment of just ₹18 lakhs.

Can you imagine this? So, the high point is that you can start small but start early.

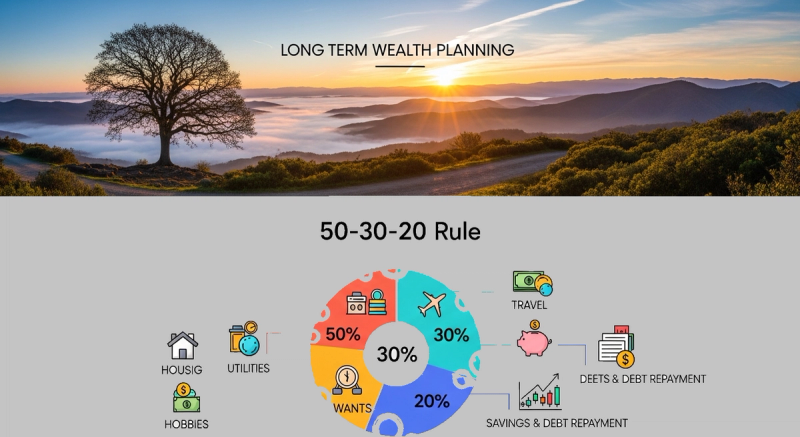

Step 4 (Follow the 50-30-20 rule)

Budgeting may sound very tedious, but the point is that at the end of the month, you should not be in a situation where you are saying, “Where did all my money go?” Rather, you should tell your money where to go, and managing personal finance is the Key. Here comes the rule that can be followed by beginners —

- 50% of income should go towards your basic needs like rent, electricity, groceries, etc.

- 30% of income should go towards your desires.

- 20% of income should be for your savings and investments.

Once you start following this, you will feel protected and financially secure, ready to face challenges. In any case, you need to understand that Long term investment is highly important.

Step 5 (Protect what you are building)

Never rely on a single investment. One serious illness can compel you to break your investments made so far, so you have to be ready for that as well.

Always have good health insurance that covers hospitalization expenses for your family. Also, if you have any dependents, opt for a term insurance cover as well in order to create a safety net, so that in case of any emergency, you should not have to look for the money that you are saving for your retirement.

Always Remember

When you talk about long-term wealth planning, consistency is better than the amount. You do not need to be perfect with money at all times, but just keep something saved that you initially decided for investment and never think of withdrawing it early.

Just as you plant seeds and wait for the tree to give you fruits after a long wait, similarly, start investing and wait to see what wonders can happen with your money. Mutual fund investment or SIP investment could be a good beginning for you.

The only advice here would be — start today if you haven’t done it yet, even if it is with just ₹500, but START!