How to Manage Your First Salary Wisely

How to Manage Your First Salary Wisely

Our first salary is more than just money credited to our bank account.

The temptation to celebrate it is speechless. After all, we have worked hard to reach this point. People may want to buy a new phone, give a treat to our family and friends, upgrade our wardrobe, or enjoy experiences that were previously out of reach.

Although there is nothing wrong in rewarding ourselves, but we should understand that our first salary is also an opportunity to build healthy financial habits that can benefit in upcoming years

The way we manage our first salary often influences how we handle money in the future.

Why The First Salary Matters

Most of us focus on how much we earn. However, financial success depends less on income and more on how the income is managed.

Two people earning the same salary can end up with very different financial outcomes. One may consistently save and invest, while the other struggles with debt despite earning a good income.

Our first salary is the perfect time to establish habits that support long-term financial stability.

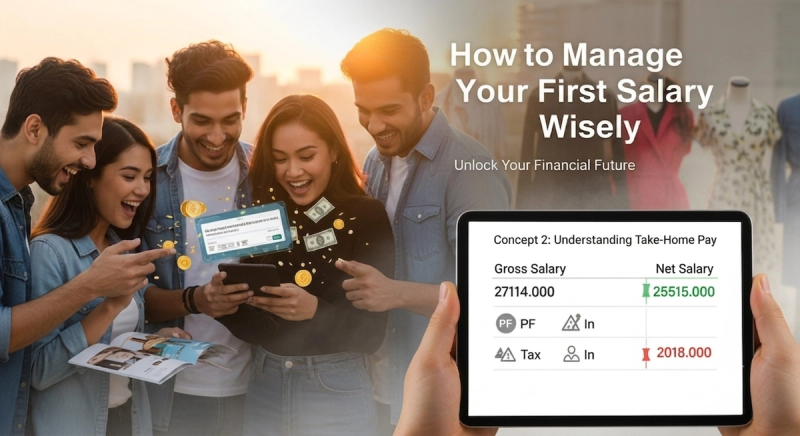

Step 1: Understand Your Take-Home Income

Before making further plans out of the salary, understand exactly how much amount will actually be credited to our bank account.

Many first-time employees are surprised when they see their actual salary credit and finds that it is lower that what was mentioned in their accepted offer letter.

There are various deductions before calculating the net salary -

- PF contributions

- Professional taxes

- Income tax deductions

- Insurance contributions

Knowing the actual monthly income helps us create a realistic financial plan.

Step 2: Create a Simple Budget

A budget is not about restricting yourself. It is simply a plan for your money.

Without a budget, it's easy to lose track of spending and wonder where your salary disappeared by the end of the month.

Start by dividing your salary into three categories - Essentials, Savings & Personal Spending.

Step 3: Pay Yourself First

One of the most powerful financial habits is saving before spending.

Many people make the mistake of saving whatever is left at the end of the month. Unfortunately, if we follow this, there are high chances that very little will be left.

Even if you start with saving just 10% or 20% of your income, but what’s important is treating these savings like a mandatory expense.

Step 4: Build an Emergency Fund

Life is unpredictable.

Unexpected medical bills, job changes or family emergencies, can create financial stress if you are not prepared.

An emergency fund acts as your safety net.

As a beginner, focus to create emergency fund equivalent to at least 3 months of essential expenses. Gradually work toward building a fund that covers upto six months of living expenses.

Step 5: Avoid Lifestyle Inflation

A common mistake among young professionals is increasing expenses as soon as they start earning.

Suddenly, expensive restaurants, frequent online shopping, and unnecessary upgrades become part of our routine.

While it's natural to enjoy our earnings, continuously increasing spending can prevent from building wealth.

Just because we can afford something doesn't mean we should buy it immediately.

Step 6: Learn the Difference Between Needs and Wants

One of the most important thing here is to understand the difference between what we need and what we want.

A need is something essential for daily living like food, rent, transportation, healthcare etc

A want is something that improves comfort or enjoyment but is not necessary like premium gadgets, designer cloths, luxury items etc.

And before making any purchase, we should first ask ourselves that do I really need this, or do I simply want it right now?

This simple question can actually save a significant amount over time.

Step 7: Start Investing Early

Many people believe investing is only for those with high incomes but that’s not true.

One of the greatest advantages with first salary people is time.

Even small investments can grow significantly through compounding when given enough time.

The important thing is to develop the habit of investing regularly.

Step 8: Avoid Unnecessary Debt

Our first salary may make it easier to qualify for loans and credit cards.

But we should always avoid taking loans simply to fund lifestyle purchases as that may create financial stress in long term.

Before borrowing money, ask -

- Is this purchase necessary?

- Can I save and buy it later?

Always think thrice before borrowing as that way we can save our future income.

Step 9: Set Your First Financial Goals

Saving becomes easier when you have a purpose.

Financial goals give direction to your money.

Start by creating short term goals that may include building a fixed amount of emergency fund, buying a laptop or something like that.

When the goals are clear, we stay motivated towards reaching them.

A check in towards our First Salary

While it's important to celebrate our achievement, it's equally important to make thoughtful decisions with our money.

Create a budget, save consistently, build an emergency fund, avoid unnecessary debt, and start learning about investing early.

And nowhere a high income is a mandate to become financially successful.

What matters most is developing the right habits from the beginning.

The financial choices made with first salary can influence the future for the coming years.

Start wisely, stay consistent, and allow time to work in our favor.